Euroscape 2024: AI Eating Software

The Accel 2024 Euroscape was unveiled earlier today at SaaStock in Dublin and you can view the full presentation here.

*********************

AI - the main driver of value creation in the tech world

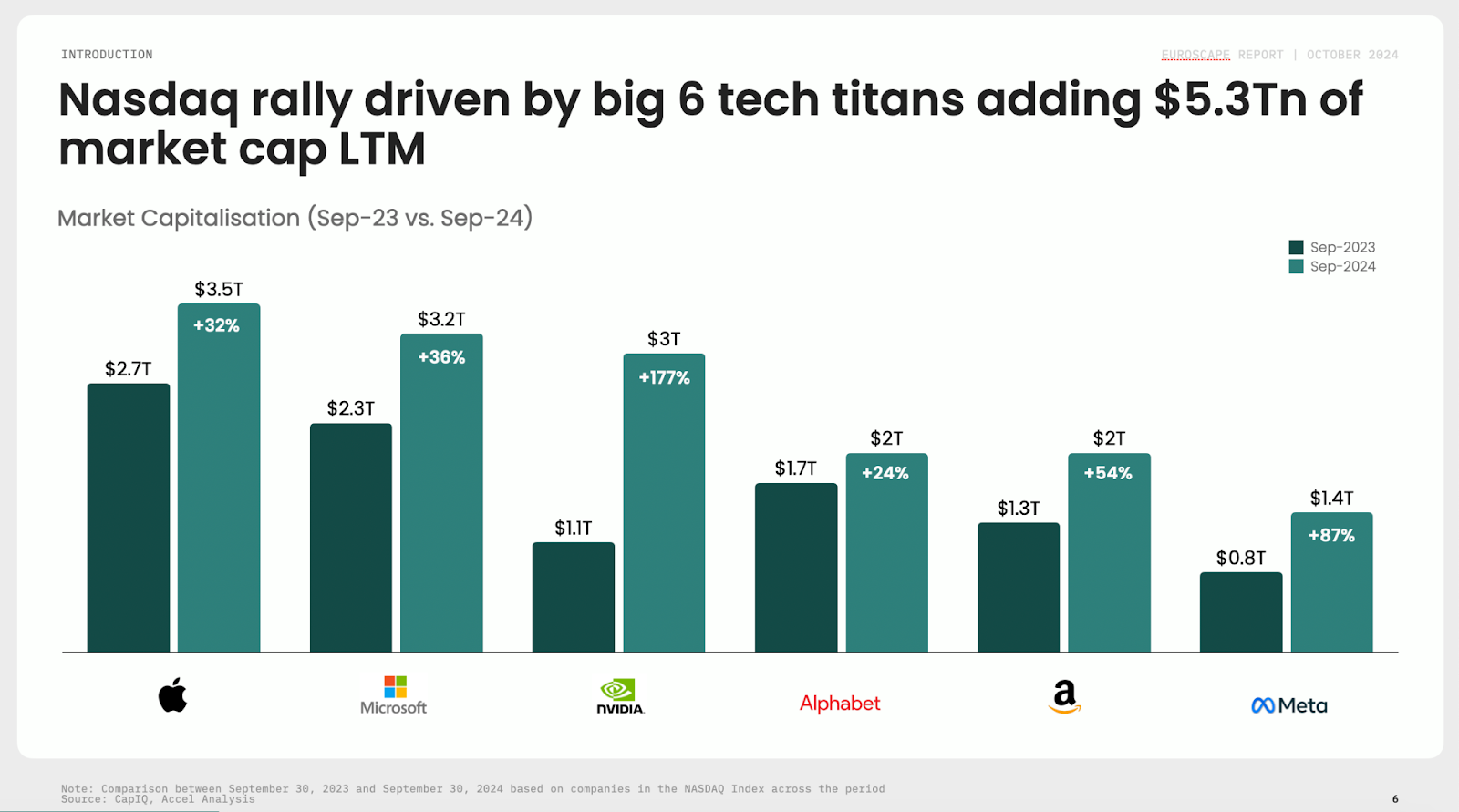

AI is rewriting software - literally and figuratively. The NASDAQ keeps climbing higher, up 38% in the last 12 months and beating new all time highs. Out of the $8.4T of value created in the past year, $5.3T is coming from the six tech titans that are investing tens of billions into AI: Apple, Microsoft, Google, Meta, Amazon and Nvidia. As AI is starting to unlock an unprecedented wave of productivity improvements across the enterprise, the development of this new tectonic shift seems unstoppable.

However, outside of the world of AI, the perspective isn’t as bright, with shadows of geopolitical uncertainties and the risk of recession looming.This environment combined with the digestion of 2020/21 high software spend and the shift of enterprise IT budgets to AI has been hard on both public and private cloud companies, putting huge pressure on growth. The Euroscape Index of public cloud companies has progressed at half the pace of the Nasdaq and the average growth rate shows a decline from 47% at their peak in Q2 2021 to 15% in Q3 2024. In 2021, 23 companies in the index were growing more than 40% per year compared to none today. The era of high software growth is fading away and leaves companies no other choice but to focus on profitability.

In this context, the cloud IPO market shows little signs of reopening. However, M&A activity remains solid, with 2024 already above 2023 at $58.7B. The M&A market remains driven by very large deals, with Synopsys’ acquisition of Ansys for $35B being the largest this year so far. The big tech titans are still missing in action, constrained by intense regulatory pressure and their focus on AI. The take private activity also remains healthy with 2024 on track to reach $40B, which is in line with 2023.

AI investments pushing venture funding back up

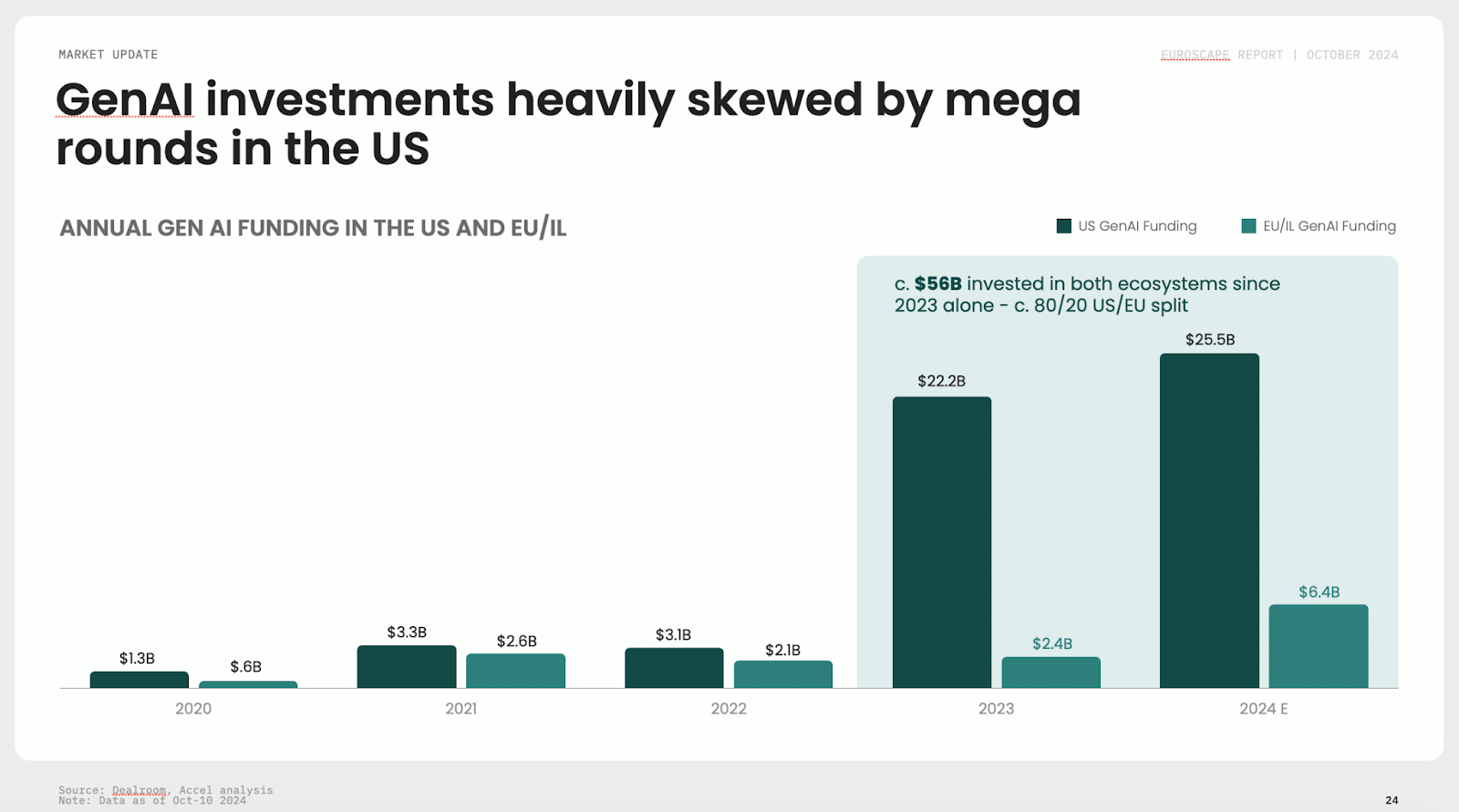

After three years of consecutive decline, funding of private AI and cloud companies across the US and Europe is climbing again at $79B, up 27% vs. 2023 and 65% vs. 2020. With AI making up $32B (40.3%) of this number and driving the majority of growth, non-AI funding is now tracking 2020’s levels at $47.3B.

When we zoom in on venture AI financing, three facts are striking:

US is leading the AI race: out of the $56B invested in 2023-24, roughly 80% has gone to US companies vs. 20% for Europe and Israel

The investments are heavily concentrated with ⅔ of the funding going to the top 6 companies in each region

⅔ of the funding has been invested in companies building foundation models

These numbers reflect the expectation of the venture community that a limited set of 12 or so companies will generate tens of billions of dollars of value in the next 5-10 years to justify these levels of investments. With OpenAI recently valued at $150B+ on the back of record breaking revenue growth, we don’t expect the flow of investments to slow down in the short term.

As billions of dollars are being put to work, the pace of development of new models is increasing, evolving from text to multi-modal, the performance of the model is increasing across all benchmarks and the cost of inference is pushed down drastically - eg. the cost of inference for 1,000 tokens on GPT4 has gone down 90% from March 2023 to May 2024. Huge progress is also coming on the text to video creation side with impressive previews from Google and Meta and Black Forest Labs (the team behind Stable Diffusion) expected to release a new video model in the coming quarters.

Game of AI thrones

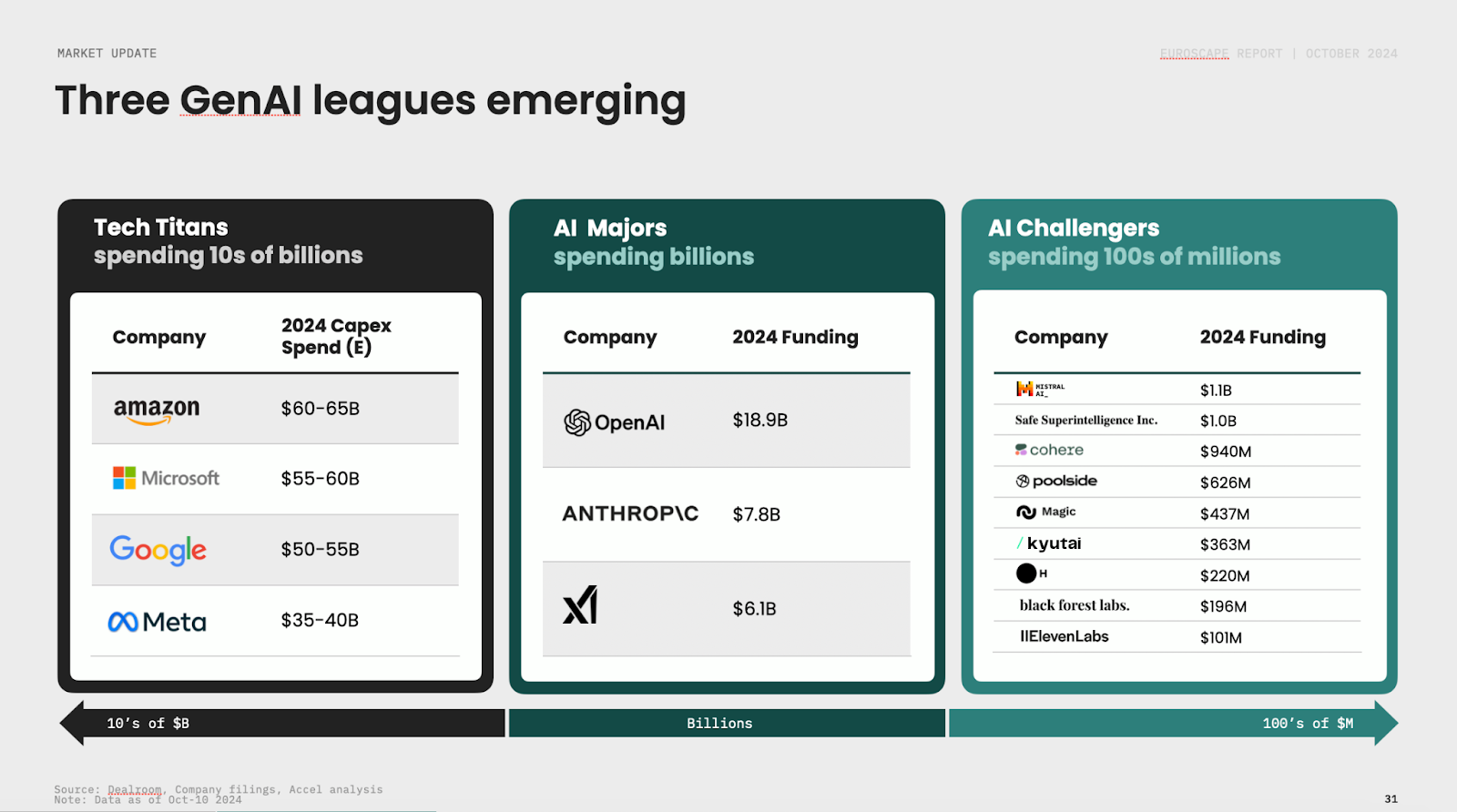

Will AI foundation models be a “winner takes all” market? Probably not. While Microsoft has a strong head start with its relationship with OpenAI, we are just in the very early innings of the race and it is too early to call it. If we look at the world today, there are three AI leagues:

The Titans: Amazon, Microsoft, Google and Meta, investing each $30-60B in AI per year, including capex

The Majors: OpenAI, Anthropic and X, each spending billions of dollars per year

The Challengers: a small number of scale ups (eg Cohere, H, Mistral,, Black Forest Labs etc…) each spending 10’s to 100’s of millions per year

It will be interesting to see in the coming months if investment capacity is the only driver of success or if more focused models and workflows can take the lion’s share of specific markets. In many applications and in particular in everything touching enterprise workflow automation, cheap inference costs and very low latency are key requirements, leading us to think that more focused models will play a significant role in the future.

The rise of Enterprise Agentic workflows

Text focused models have started to impact the productivity of enterprises primarily on the software development side, improving productivity of developers by 20%+, on the customer support side, dramatically deflecting the number of contacts managed by humans (numbers we are hearing are in the 20-40% range and increasing) and on the media creation side. Next to these use cases already in production, most large enterprises have been experimenting with internal applications and expect to deploy them next year.

We expect the next generation of models to include agents specifically trained to execute business tasks and workflow. These models will generate a new wave of automation for enterprises as AI will handle the execution of more complex tasks and tasks with a large number of possible outcomes that current automation tools are struggling to address. Initial announcements have been made by Microsoft and we expect new releases in this field next year and enterprises to start experimenting with them. One challenger to watch is H, the foundational companies focusing on agentic workflow who received investments from UiPath and is expected to release their first product in the coming months.

The top 100 2024 Accel Euroscape winners

As AI dominates the cloud world, it is not surprising to see a big shift in the list of winners this year. We’ve also adjusted the categories to reflect the new landscape of AI driven business models. You can see the full list and more in the report here

************************************************

At Accel, we can’t be more excited by the trends we are seeing around AI and the new generation of AI-native applications that will be created in the coming years. We believe this secular trend will continue for the foreseeable future and redefine the way application and software will be written. We have been very active in the category with investments in Scale, Synthesia, H, Decagon, Assembly, Ema, Gamma, Vercel among others and expect a large part of our new investments to fall in this category.

We’ve deployed more than $10B across 400+ AI & cloud companies in the past four decades and have been fortunate to partner with many exceptional cloud & AI founders globally. While there is still an imbalance today between the US and Europe on AI, we expect eventually that this difference will flatten and that AI winners will come from anywhere, like we have seen for cloud companies: from Atlassian in Australia to UiPath in Romania, Celonis in Germany, Snyk in Israel, and Docusign and Crowdstrike in the US. We can’t wait to see what the next decade will bring.

No comments:

Post a Comment